Are We Controlling Costs — or Designing Value?

The New Frontier of Financial Profitability

Last October, the CFO of a mid-cap consumer goods company in Mexico City leaned back in his chair, pushed a spreadsheet across the table, and said something I've heard too many times: "Corporate just handed us a 15% opex cut. But nobody told us what to invest in next."

He wasn't being dramatic. He was describing a structural failure.

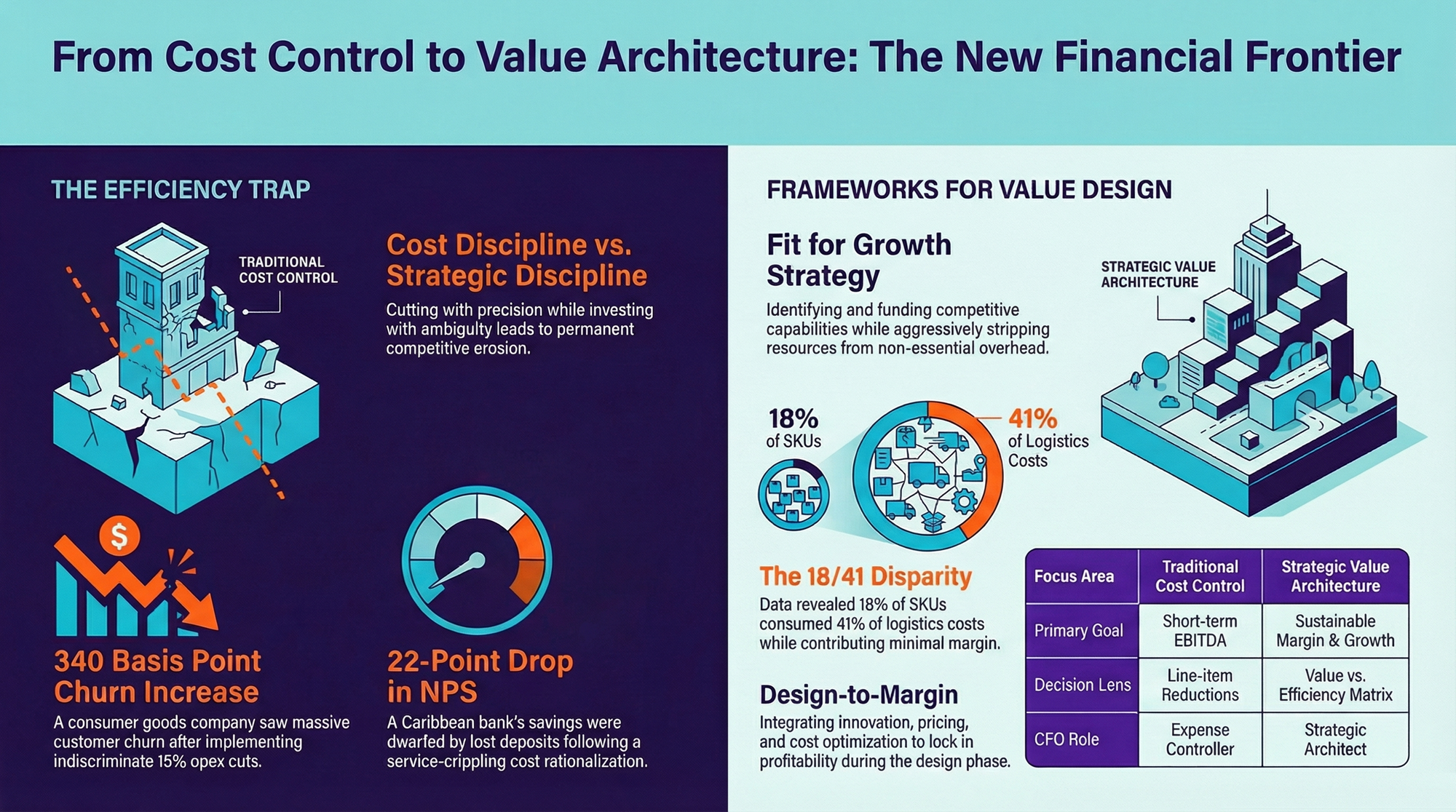

His company had just completed a six-month cost-reduction program. Headcount down 12%. Travel budgets slashed. Two R&D projects frozen. The EBITDA looked better — for exactly one quarter. By Q2, customer churn in their premium segment had climbed 340 basis points. Their most profitable product line was losing shelf space to a competitor that increased its marketing spend during the same period.

I've seen this pattern across Latin America, the Caribbean, and beyond: organizations that confuse cost discipline with strategic discipline. They cut with precision but invest with ambiguity. The P&L improves temporarily. The competitive position erodes permanently.

As Oracle has noted, persistent uncertainty has elevated the CFO's mandate — not just to cut costs, but to determine which growth investments actually deserve capital. The question isn't whether to be efficient. The question is whether efficiency alone can sustain you.

It can't!!!

Three questions should frame this conversation:

When does cost reduction become self-defeating? At what point do "smart cuts" start destroying the capabilities that generate margin?

What frameworks connect cost structure to value creation? How do high-performing organizations decide what to cut and what to fund — simultaneously?

How must the CFO's role evolve to architect value rather than simply control spend?

I. The Efficiency Trap: When Cutting Becomes the Strategy

Indiscriminate cost reduction creates a dangerous financial illusion: immediate EBITDA improvement that masks a gradual erosion of competitive capacity. A Wharton study puts it plainly — a permanent challenge for CFOs is balancing spend and investment without damaging competitiveness.

The evidence is unambiguous. During 2020–21, companies across sectors slashed R&D and marketing budgets to protect short-term earnings. Many were forced to reverse course within 18 months after watching revenue growth collapse. By focusing exclusively on costs, they lost sight of the fundamental value drivers that sustained their market position.

I made this mistake early in my career. In 2009, I worked with a Caribbean bank to design a cost rationalization program that looked elegant on paper — consolidating back-office operations, reducing branch staffing, and renegotiating vendor contracts. Total savings: $4.2M annually. What we didn't model was the impact on service quality. Within 14 months, the bank's Net Promoter Score had dropped 22 points. The deposits they lost dwarfed the savings.

That experience fundamentally changed how I approach cost programs. Now, when I advise clients, I prioritize modeling the downstream impacts on service and growth. That means running sensitivity analyses alongside financial projections, linking cost reductions to operational metrics like customer churn, service wait times, and client satisfaction. I push for pilot-testing significant cuts in select regions before rolling them out — to quantify unintended consequences before they become irreversible. And most importantly, I bring cross-functional teams from operations and customer service into the room early, to stress-test assumptions that finance alone can't see.

Efficiency is not the opposite of investment — it's a precondition for smarter investment.

Kevin Rasmus at Accenture has formalized this insight into what he calls design-to-margin: a discipline that integrates product innovation, pricing strategy, and cost optimization, ensuring every offering is engineered for its target margin from conception. It's not about spending less. It's about spending with intent.

II. Four Frameworks That Connect Cost to Value

Against the reductionist view of costs as line items to minimize, several integrative frameworks have emerged. Each addresses a different dimension of the cost-value equation:

Fit for Growth (PwC / Strategy&) connects growth strategy directly to cost transformation. The logic is surgical: identify which capabilities set you apart competitively, fund them aggressively, and strip resources from everything else. As the framework's architects describe it — cut corporate fat and build competitive muscle simultaneously. In Latin America, where conglomerates often carry bloated shared-service structures inherited from decades of acquisition, this framework is particularly relevant. We applied it with a multi-country retail group based in Guatemala, reallocating 23% of their SG&A from administrative overhead into supply chain analytics and category management. The result: a 180-basis-point margin improvement within three quarters.

Strategy That Works (Leinwand & Mainardi) identifies five unconventional practices for closing the strategy-execution gap. The most powerful: committing to a coherent identity — aligning value proposition, capability system, and portfolio so that every dollar spent reinforces the same strategic logic. Apple and IKEA are the textbook examples. In our region, I'd point to Mercado Libre, which has relentlessly invested in logistics infrastructure while competitors optimized for short-term marketplace commissions.

Design-to-Margin integrates customer-centric innovation, contextual pricing, and intelligent operations to lock in profitability from the design phase. In practice, this means analyzing total cost and price sensitivity simultaneously throughout the product development cycle — not bolting on a margin target after the product is built.

Cost-to-Serve quantifies the complete cost of serving each customer — logistics, sales, service, returns — to expose which products or segments are silently destroying value. Recommended by Deloitte as a foundational profitability tool, it provides the transparency that traditional P&L structures obscure. In a retail engagement in the Dominican Republic, applying cost-to-serve analysis revealed that 18% of the client's SKU portfolio accounted for 41% of logistics costs while contributing less than 6% of gross margin. That data transformed the assortment strategy overnight.

These frameworks aren't academic exercises. In real engagements, they become the operating language between the CFO, the COO, and the business unit leaders. In a recent session with a retail client's executive team, the CFO opened the conversation by asking: "What if we stopped focusing only on cutting headcount? Where should we be doubling down instead?" The COO identified a logistics process that, despite its cost, was essential for last-mile customer satisfaction. Rather than debating further reductions, the team redirected resources from back-office automation to that logistics function. Finance, operations, and sales leaders mapped — together — which activities genuinely drove growth and which were candidates for streamlining or outsourcing. The conversation shifted from "how much can we save?" to "where will each dollar make the most difference?" That's the moment the organization starts designing value.

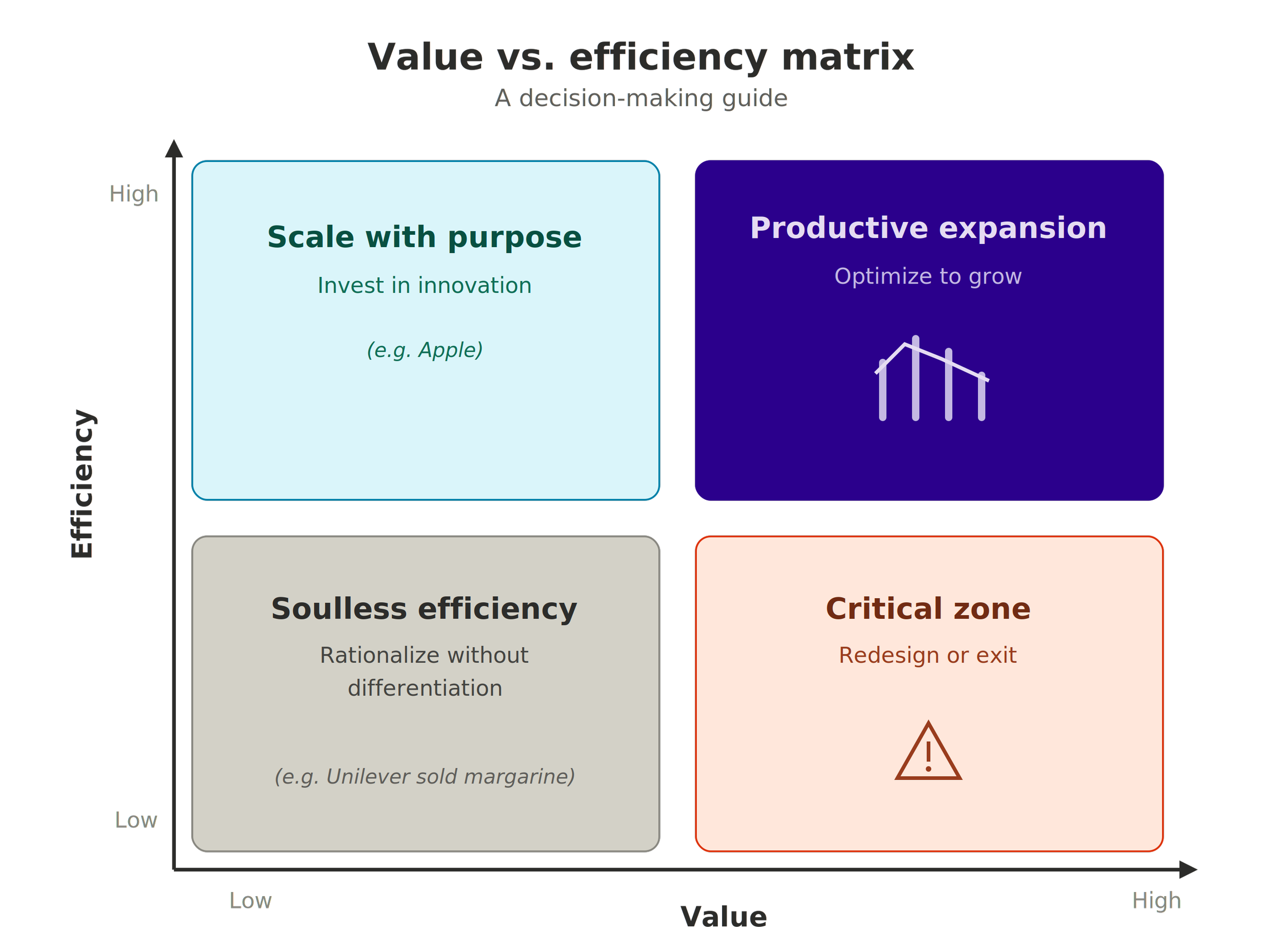

To synthesize these four frameworks into a single decision lens, I use a Value vs. Efficiency matrix with my clients. The logic is simple but disciplined:

Every initiative in your portfolio should sit somewhere on this matrix. If you can't place it, you don't understand it well enough to fund it.

III. Evidence: Who's Getting This Right?

Unilever rejected a hostile bid in 2017 and used the pressure as a catalyst. They committed to aggressive margin targets, divested low-growth businesses (margarine and spreads), and reinvested the proceeds in personal care brands and innovation. Earnings per share improved materially. The lesson: divesting low-value activities to fund high-potential ones isn't retreat — it's portfolio architecture.

Pfizer completed the sale of its 7.3% stake in Haleon (the consumer health spinoff with GSK) in early 2025 for approximately $3.24 billion. The proceeds went directly into strengthening its core biotechnology pipeline. As Pfizer's CFO described it, the divestiture was executed methodically to reinforce financial stability while doubling down on higher-value therapeutic areas.

Santander announced in late 2024 the closure of 95 branches in the UK (21% of its network) and 18 in the US (4.5%), signaling a decisive bet on digital transformation. Simultaneously, it sold 49% of its Polish subsidiary to Erste Bank for €6.8 billion, generating approximately €2 billion in gains. Those resources are now funding Openbank and new digital services — replacing legacy infrastructure with scalable platforms.

Leading retailers across the region are deploying advanced analytics to align inventory, assortment, and pricing with value creation. Data science for demand prediction allows them to reduce costs without compromising customer experience. The common thread: design value first, then optimize cost — never the reverse.

IV. The CFO as Value Architect

The daily tension is real. Every CFO I work with lives in the gap between containing costs and funding the future. The question that comes up in almost every engagement: "If we cut headcount or cancel key projects, how do we maintain competitiveness in 24 months?"

The frameworks above are shifting financial discourse toward more holistic value metrics. Oracle emphasizes that an integrated approach — supported by modern ERP systems and advanced analytics — enables organizations to precisely identify where to reduce costs without sacrificing the capital required for strategic investments.

This evolution is redefining the CFO's role: from controller to strategic architect, working in close collaboration with marketing, operations, and sales to prioritize investments that maximize sustainable return.

A practical recommendation I give to every finance leader: deliberately include all functional areas in the cost-investment conversation. Finance alone cannot visualize the full value potential of the business. Dialogue with line directors reveals critical insights — for example, recognizing certain supply chains as strategic investments rather than cost centers.

To operationalize this, I recommend establishing a recurring "Value Council." Bring together finance, operations, marketing, sales, and HR leadership for structured quarterly sessions devoted to strategic resource allocation. The agenda covers three things: (1) a rapid review of current cost programs and investment proposals, (2) roundtable identification of value-driving projects across departments, and (3) cross-functional assessment of risks or unintended consequences tied to proposed cuts. Facilitate with a standardized template that maps costs to value drivers for each major initiative. Every department's perspective shapes the decision — not just finance's.

In multiple transformation engagements, we've applied what Strategy& calls end-to-end transformation: analyzing the entire value chain before determining any cost adjustment. This comprehensive approach ensures that efficiency initiatives don't compromise the fundamental drivers of value creation.

Profitability doesn't come from spending less. It comes from knowing — with surgical precision — where every dollar creates value and where it doesn't. The organizations that master this distinction don't just survive downturns. They use them to widen the competitive gap.

Five Actions for Monday Morning

1. Redesign your P&L by strategic function. Stop treating all expenses equally. Separate support activities (candidates for efficiency) from value-driving activities (innovation, customer experience, strategic supply chain). This single reframe changes every budget conversation.

2. Deploy cost-to-serve and customer profitability analysis. Allocate resources where they generate the highest margin. Consider divesting commoditized, low-growth products that consume disproportionate operational resources. If 18% of your SKUs eat 41% of your logistics budget, you have your starting point.

3. Build a value culture — not just a cost culture. Involve marketing, operations, and finance in continuous business model review. As one CFO told me last year: "We need metrics that measure value creation, not just cost savings." Train your finance team to see beyond the traditional P&L — track customer lifetime value, innovation ROI, NPS, employee engagement, and share of wallet alongside the standard financial indicators.

4. Invest in analytical capabilities. Leverage advanced analytics and modern ERP platforms to simulate investment-versus-cut scenarios. Predictive models can reveal how certain expenditures catalyze future revenue — justifying the initial investment with data rather than intuition.

5. Prioritize financial sustainability over quarterly optics. Maintain a dynamic balance between liquidity (intelligent cuts) and growth (investment in differentiated value). The new profitability is born from designing differential value before optimizing existing processes. The future belongs to organizations that create differentiated value propositions and scale them efficiently — not to those who indiscriminately cut expenses and hope the market doesn't notice.

In 12 to 24 months, the companies that invested through this cycle — with discipline, with frameworks, with clear cost-to-value mapping — will be the ones setting prices, not chasing them.

About the Author

Pedro San Martín is Principal at Asher & Company, Strategic Finance Center of Excellence in partnership with PwC Interamericas. He chairs the IMA Profitability & Cost Management SIG and teaches at ITAM and Universidad Anáhuac. Contact: psanmartin@asheranalytics.com

Ready to redesign your profitability architecture? Schedule a Discovery Call at asher.company/contact

References

Oracle. (2024). "The Elevated Role of the CFO." oracle.com/erp/finance

Henisz, W., & Zelner, B. (2023). "Balancing Spending and Investment." Wharton School, University of Pennsylvania.

Rasmus, K. (2024). "Design-to-Margin: A New Operating Discipline." Accenture Strategy.

Vinay Couto, John Plansky, & Deniz Caglar. Fit for Growth: A Guide to Strategic Cost Cutting, Restructuring, and Renewal. PwC Strategy&.

Leinwand, P., & Mainardi, C. (2016). Strategy That Works: How Winning Companies Close the Strategy-to-Execution Gap. Harvard Business Review Press.

Deloitte. (2024). "Cost-to-Serve Analytics for Consumer Industries." deloitte.com

Pfizer Inc. (2025). "Haleon Stake Divestiture — Q1 Investor Update." pfizer.com/investors

Santander Group. (2024). "Branch Network Optimization and Erste Bank Transaction." santander.com/investors

Napolitano, J. (2023). "Profitable Growth." Corporate Finance Institute.