Profitability Without an Owner: Why Banks Fail Where It Matters Most

During a quarterly board session with the executive team of a regional bank — headquartered in Miami, operating across five Caribbean islands — the Chief Strategy Officer broke a long silence with a sentence I haven't been able to shake:

"We track growth. We don't track profitability — at least not in a way that matters."

It wasn't a scandal. It was routine. And that's what made it worse.

The bank had all the appearances of momentum: new branches in Nassau, a growing mortgage book in San Juan, a mobile app gaining traction with younger users in the Dominican Republic. But when I sat down with the profitability dashboard, none of those wins connected to anything financial in a meaningful way. Profitability was a number someone printed once a month. Not a process. Not a discipline. Certainly not something anyone in the room felt personally responsible for.

So I asked: "Which of your strategic projects has actually improved return on assets?"

The CFO looked at the COO. The COO looked at the transformation director. Then both looked at the CEO. Silence. Finally, someone offered: "We haven't mapped those links yet… but we're sure they're there."

I hear that phrase more than I'd like to admit….

Three questions should frame this conversation:

Why do organizations treat profitability as an outcome rather than a process?

What are the real consequences — especially in regulated industries like banking?

How can profitability management be institutionalized in a way that actually sticks?

1. Profitability Is Not a KPI — It's a Living System

Uno de los errores más frecuentes que veo en organizaciones medianas y grandes es confundir la rentabilidad con una fotografía contable. Se mide trimestralmente, se reporta a inversores, se debate en comités financieros. Pero no se gobierna como proceso. (Classic Miami Spanglish!)

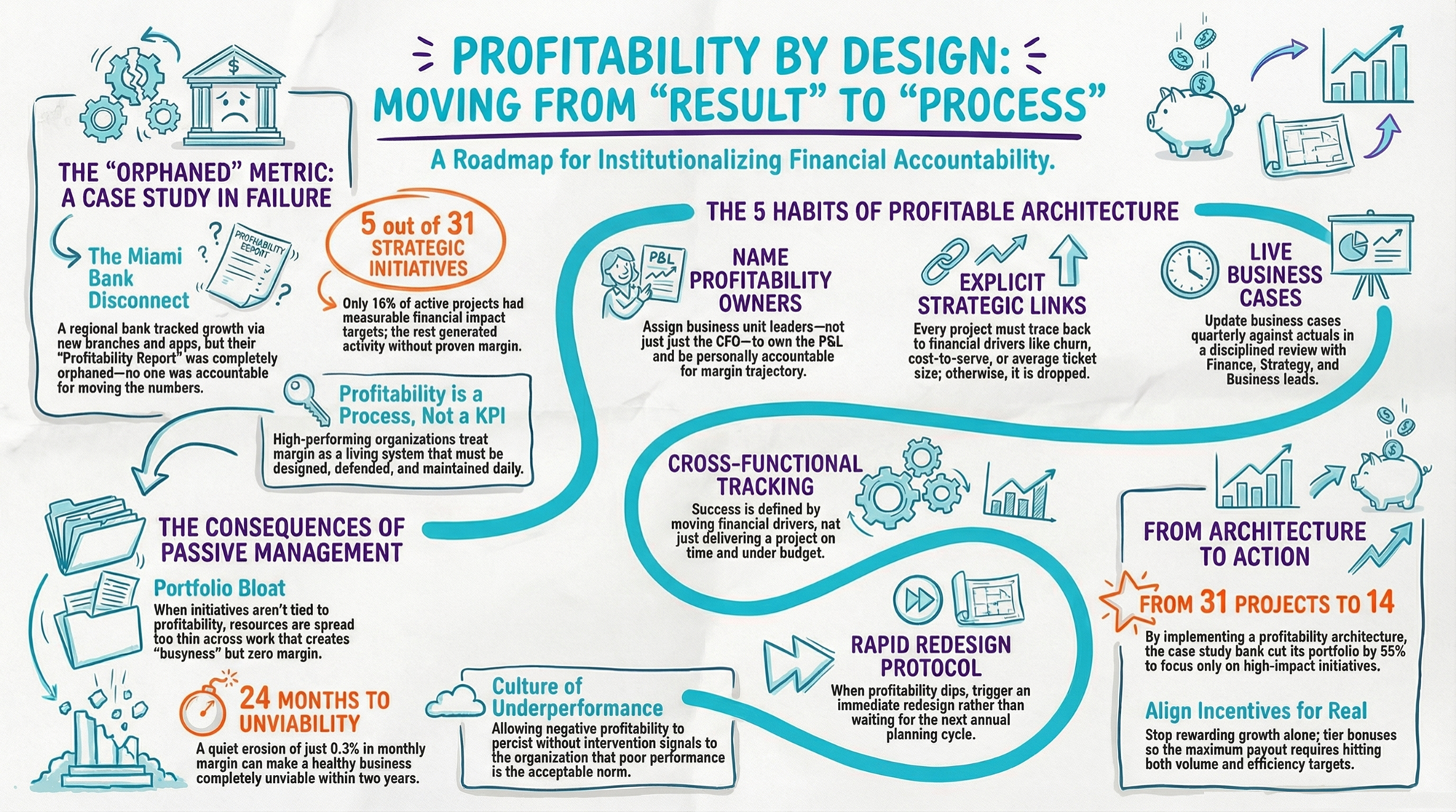

That Miami bank published a monthly "Profitability Report." It was precise. Full of figures. Beautifully formatted. And completely orphaned — no one owned it. Nobody woke up in the morning accountable for making those numbers move as part of strategic execution.

When that bridge is missing, what gets executed never transforms the profitability model. And what gets measured just… sits there. Profitability gets reported as if it were the inevitable byproduct of growth — as if nobody had to design it, defend it, or maintain it.

The bank had 31 active strategic initiatives. Only 5 had measurable financial impact targets…

Five out of thirty-one. I wish I could tell you that the ratio is unusual. In over 20 years working across 15+ countries — banking, healthcare, consumer goods — it's closer to the norm than the exception.

2. Three Consequences Nobody Talks About

Focus collapses. When profitability isn't tied to specific initiatives, the project portfolio bloats. Resources get spread thin across work that generates activity but not margin. People stay busy. The P&L doesn't care.

Inefficiency becomes invisible. Without someone actively watching profitability at the process level, things like credit approval cycle times, early-stage churn, and branch-level cost allocation — they keep running on yesterday's logic. Margins erode quietly. Nobody sounds the alarm because nobody's assigned to listen.

Underperformance becomes culture. When a business unit posts negative profitability three quarters in a row, and nothing happens — no redesign, no reallocation, no hard conversation — you've just told the entire organization that poor performance is acceptable. "That's just how things work here." At a 0.3% monthly erosion rate, a healthy business becomes unviable within 24 months. There's no single moment of alarm. That's the danger.

Profitability doesn't announce its departure. It leaves quietly.

3. What High-Performing Organizations Actually Do

The banks and companies I've seen sustain profitability through complexity and regulation aren't lucky. They share five structural habits:

They name profitability owners. Not the CFO running a year-end ROI calculation. Each business unit has someone — a business leader with a financial lens — who owns the P&L and is personally accountable for margin trajectory. This is a leadership role, not a reporting function.

They connect profitability to strategy — explicitly. Their OKRs trace back to financial drivers. If an initiative can't demonstrate a clear link to margin, volume, ticket size, churn, or cost-to-serve, it doesn't make the portfolio. Full stop.

They keep business cases alive. Every initiative has a business case that gets updated quarterly against actuals — not defended once at approval and forgotten. The review typically brings together the business unit lead, Finance, and Strategy in the same room. They compare forecasted versus actual margin impact, revisit assumptions, and assign corrective actions on the spot. It's disciplined, not ceremonial.

They track across functions. Finance and Strategy don't operate in parallel universes. An initiative isn't "successful" because it delivered on time and under budget. It's successful if it moved a key financial driver. Operational results and financial returns get reviewed at the same table.

They react fast. When a unit stops being profitable, they don't write a narrative explaining why the numbers are what they are. They trigger a redesign protocol. Speed matters because that 0.3% monthly erosion doesn't wait for the next planning cycle.

4. Five Steps to Get Started

People ask me all the time: "Where do we begin?" Here's the path I recommend — not because it's the only one, but because I've seen it work.

Step 1: Name a profitability owner. Every business unit needs someone who knows its P&L cold. Not the controller. A business leader who thinks about margin improvement the way a commercial leader thinks about a pipeline. If nobody's name is next to the number, nobody's moving it.

Step 2: Map initiatives to profitability drivers. Take your current strategic portfolio and force-link each initiative to a specific driver: margin, volume, average ticket, churn, cost-to-serve. If you can't make the link, the initiative needs to be rethought — or dropped.

Step 3: Create a quarterly profitability review. You have already reviewed revenue. You have already reviewed the sales pipeline. Build a standing forum with the same rigor for profitability — by unit, channel, and segment. Make it uncomfortable to show up unprepared.

Step 4: Put profitability on the strategic dashboard. If it's not visible where the executive team makes decisions, it's not a priority. This sounds obvious. It almost never happens by default.

Step 5: Align incentives — for real. If bonuses reward only growth, you'll get volume at the expense of efficiency. Consider a tiered structure: one portion tied to profitability targets (reducing cost-to-serve, improving net margin), another to responsible growth (acquisition, retention). Maximum payout goes to teams that hit both. That's how you stop optimizing one metric at the expense of the other.

From KPI to Organizational Discipline

Six months after that board session in Miami, the bank made a structural move. They created a new role: VP of Integrated Profitability. They cut their strategic portfolio from 31 initiatives to 14 — every one of them with a measured financial impact. For the first time, the annual plan included margin simulations and cash flow modeling as core inputs, not appendices stuffed at the back.

It wasn't magic. It was a purpose — followed by a clear process to back it up.

Profitability is not a destination. It's an architecture. And like all architecture, it needs blueprints, owners, materials, inspections, and maintenance. The organizations that understand this don't just survive disruption and regulation. They come out stronger on the other side.

About the Author

Pedro San Martín is Principal at Asher & Company, Strategic Finance Center of Excellence in partnership with PwC. He chairs the IMA Profitability & Cost Management SIG and teaches at ITAM and Universidad Anáhuac.

Contact: psanmartin@asheranalytics.com

Ready to map your profitability architecture? Schedule a Discovery Call at asher.company/contact

Profitability by design

References

Bradford, R. (2024). "How Profitability Drives Bank Performance."Empyrean Solutions. empyreansolutions.com/blog-profitability-transforming-financial-institutions/

Oracle Financial Services. "Financial Services Profitability Management."oracle.com/financial-services

Empyrean Solutions. "Profitability Measurement & Analysis." empyreansolutions.com/performance-management/profitability/

Strata Decision Technology. "A Resurgence of Profitability Analysis for Financial Institutions." stratadecision.com

FIS Global. "Financial Services Profitability Manager." fisglobal.com

Xu, T., Hu, K., & Das, U. (2019). "Bank Profitability and Financial Stability." IMF Working Paper No. 19/5. imf.org/en/publications/wp/issues/2019/01/11/bank-profitability-and-financial-stability-46470

Hoxha, A., Bajrami, R., & Prekazi, Y. (2025). "The Impact of Internal and Macroeconomic Factors on the Profitability of the Banking Sector: A Case Study of the Western Balkan Countries." Business: Theory and Practice, 26(1), 28–47. DOI: 10.3846/btp.2025.18670

NetSuite. "Profitability Forecasts: What They Are and How to Create Them." netsuite.com

Napolitano, J. (2023). "Profitable Growth." Corporate Finance Institute. corporatefinanceinstitute.com