The Uncollectible Promise

Why technology and AI so often fail to create value in the CFO’s office — and what to measure instead

The figures in this article are illustrative, drawn from patterns I have seen in practice. They do not represent any specific client.

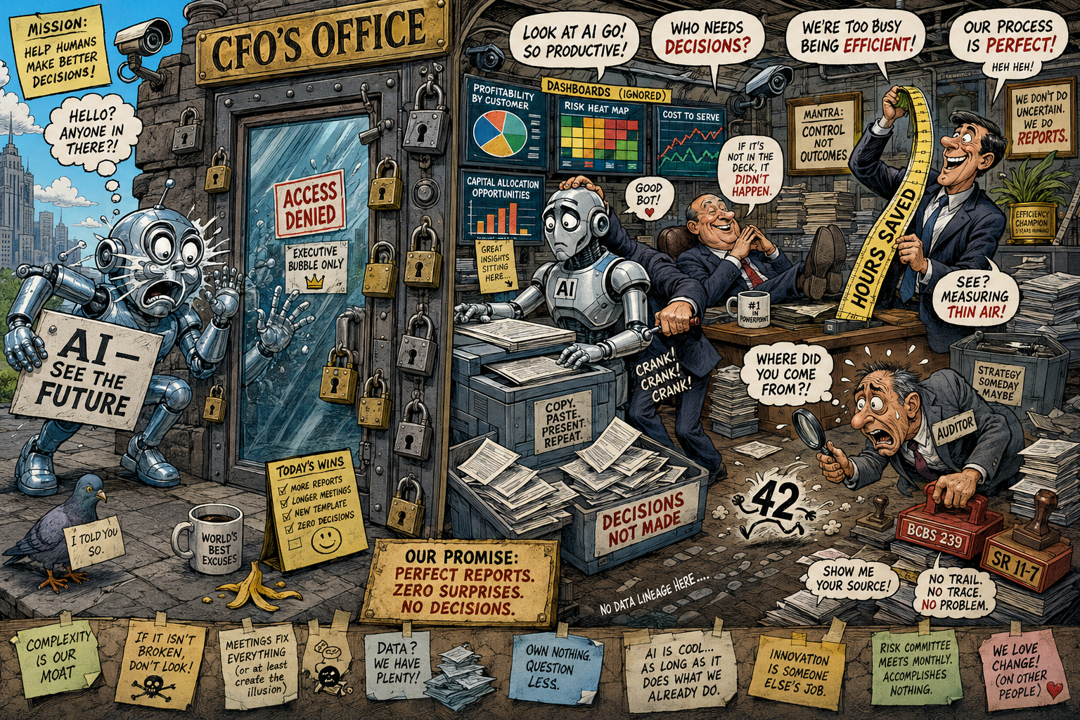

A finance chief walked me through his dashboard. Trained forecasting models. Nightly anomaly detection. An assistant that drafted variance narratives in seconds. He had spent real money on it. Before I congratulated him, I asked one question.

“How many committee decisions changed last quarter because of something that came out of here?”

He paused. The FP&A director looked at the ceiling. Then the CFO answered, a little uncomfortable: “None that I can remember. But we close faster, with fewer people.”

That is the whole problem in one sentence. He had bought the ability to see further, and he was using it to run in place.

I have watched this happen in banks, utilities, retailers, and hospitals. The technology works in the pilot. The models behave in testing. And then the payoff everyone signed up for — earlier insight, better calls, faster adaptation — never shows up. It is not a data problem or a vendor problem. It is a problem of purpose, and more precisely, of what the team chose to measure.

Three questions frame what follows:

- Why does a function built never to be surprised end up neutralizing the one thing AI came to offer?

- What should a business case measure when the real gain is not hours saved but the quality of a decision?

- How do you instrument that quality without giving up the trust, control, and traceability that finance cannot negotiate away?

1. The function built never to be surprised

The CFO’s office exists to take surprise out of the business. Reliable numbers, clean compliance, capital sitting where it should. Decades of process, controls, and habit all point the same way: no surprises. That instinct is worth defending. It is also the thing quietly strangling the technology.

AI does not remove surprise. It moves it forward in time. It hands you an earlier, cheaper signal and lets you test an assumption you used to be able to ignore. That puts finance in an odd spot — expected to be the steady hand and, at the same time, the one asking the uncomfortable “what if.” The hard part is not learning the tool. It is holding onto what works while letting go of what is about to stop working.

The numbers say the same thing. Across more than two hundred AI projects in finance, roughly seven in ten changed no core routine — not forecasting, not the close, not risk. They did not fail. They just never left the pilot.

7 in 10

AI projects in finance that changed no core routine

But some cross over, and they show what is possible. At a regional insurer, an AI claims-forecasting tool started life as a quarterly-planning experiment. Six months later it anchored every major portfolio review. It did not just automate a report — it surfaced shifts in claim types and flagged outliers worth a second look. So the team rebuilt the approval workflow around those real-time alerts, and the backlog fell. You knew it had landed when strategy discussions started quoting the tool instead of the old month-end deck.

A planning director at a utility put it better than any consultant could: “Nobody here gets promoted for doubting out loud. They get promoted for defending a number.” That is the trap. When the only work that counts is closing and defending a figure, a tool that opens up alternatives reads as noise, not help.

I have seen the trap spring open with something almost trivially small. At an industrial group we started a fifteen-minute Monday standup. Two analysts each bring one outside signal. One question on the table: “if this were the first sign of something bigger, what would it be?” The AI did the scanning; the people decided what mattered. Eight weeks in, those conversations were already bending the budget assumptions. The model did not change. Who felt responsible for looking ahead did.

So the first insight is not about technology at all. The value stalls because of how the team thinks — and how the team thinks is set, more than anyone likes to admit, by how the business case was written.

2. The business case that measures the wrong thing

Most AI business cases in finance rest on two numbers: hours saved and heads cut. How much time do we get back, how many roles come out. It feels rigorous. It measures the wrong thing — output, what the machine produces, instead of outcome, the quality of the decision that follows.

The difference matters. Sending an email is output. Closing a report is output. Training a model is output. Reaching a call that holds — that nobody has to relitigate three times — is outcome. Measure only hours, and AI will look like it underdelivered even on the days it changed the decision.

Output vs. Outcome

Output is what the machine produces. Outcome is the quality of the decision that follows — and whether it holds.

And the decision can be measured. On the teams that used AI well, the share of decision-grade communication — messages that actually push an issue to a call instead of circling it — rose from about six in ten to eight in ten among executives, and from roughly two-thirds to over four-fifths at the operating level. The email volume barely moved. What moved was the “let’s just hop on a call” reflex that used to follow every doubt. Fewer fire drills. More decisions that stuck.

One CFO changed a single question in his reviews. He stopped opening with “why did this take so long?” and started with “what did we learn that we could not have learned any other way?” It sounds cosmetic. It is not. The first question pays for speed and punishes trying anything new. The second makes the experiment part of the job instead of something you apologize for.

That same team ran an explainable forecasting model next to their usual statistical one for two sprints, changing no official guidance. It was not more accurate. It gave them something better: they found out which data they actually trusted, and where the old method was stronger than they had assumed. Nobody got charged with “wasting time.” The learning was the deliverable.

So the business case stops asking only “how much do I save?” and starts tracking four things:

- How much of the work comes out decision-grade on the first pass.

- How much the gap shrinks between a signal appearing and someone acting on it.

- How much friction disappears — fewer escalations, less rework, fewer clarification meetings.

- How many early signals actually changed an assumption, instead of just lighting up a dashboard.

A business case worth approving does not sell time back. It sells decisions that last.

3. Trust is the price of admission

Here an experienced CFO pushes back, and the pushback is fair. Measuring outcome quality sounds fine until an auditor asks for proof. Finance cannot trade trust for curiosity. It has to deliver both.

The way out is not choosing between control and exploration. It is building both into the same process. Every AI-assisted decision should reconstruct on demand: the data it drew on, the model it used, who validated it, which steps it touched, what came out. That trail is not bureaucracy. It is what lets you defend the better outcome when someone asks you to.

In Latin America this is not a nice-to-have. A model that feeds a credit or capital decision lands squarely inside the data-lineage discipline of BCBS 239 and the model-governance expectations that U.S. supervisors set out in SR 11-7 — guidance the region’s regulators, from Mexico’s CNBV to the superintendencies in Panama and the Dominican Republic, echo with their own local wrinkles. The pattern travels. In the EU, the EBA and ECB expect documented models and clear lineage; in the U.S., SR 11-7 is the framework examiners hold banks to. In every one of these markets, an outcome you cannot rebuild for a regulator is not a good outcome, however fast it came out.

Speed without lineage is a liability, not an asset.

A CFO at a mid-sized bank said it plainly to his risk committee: “I can defend a number that took a week. I cannot defend one that came out in a minute if I do not know where it came from.” Trust is not something you argue for after the fact. You build it into the process, or you do not have it.

One caution, because it is easy to miss: the measurement itself has to be as traceable as the decision. If “decision-grade communication” comes down to one analyst’s judgment on a Friday, it will not survive contact with an auditor either. Define how it is coded, keep the log, make it reproducible. The metric that proves your outcome has to clear the same bar as the outcome.

I have watched this scale the right way. At a retail group, a local team wrote an AI routine to separate real anomalies from noise in store expenses. It worked. Instead of hoarding it, they published the code and the checklist — and before it went into the standard monthly review, they set governance rules with internal audit. Nobody was ordered to use it. It was simply cleared as safe to reuse. That is how a local trick becomes a shared practice without anyone losing control.

Put simply, a business case that survives has three parts, and most have only one: the technical promise you are after, the outcome-quality indicators that prove you got it, and the traceability that protects the mandate. Drop the third and the auditor kills it. Drop the second and you are measuring what you always measured. Drop the first and there was never anything new to win.

The edge AI gives finance does not collapse in a single quarter. It leaks — a little every time a better outcome gets judged on efficiency alone and quietly shelved.

What to do Monday

Pull your most recent AI business case and read its scorecard. If every indicator is hours, cost, or volume, and not one touches the quality of a decision — first-pass calls, time-to-action, friction removed — the scorecard is too narrow to tell you whether the thing worked.

Add two indicators before your next committee. One for outcome: the share of decisions closed in the first review without escalation. One for traceability: every AI-assisted recommendation carries a short log of the data and models behind it. Both are cheap to check and easy to argue about in the room — which is the point.

Over the next twelve to twenty-four months, expect regional regulators to require the same lineage for AI-assisted decisions that they already require for data. The CFOs who built the measurement early will be ready. The ones still counting hours saved will be explaining, to a committee that has stopped being patient, why a large investment moved nothing. The differentiator was never the technology. It was the choice of what to measure.

Pedro San Martín

Principal · Strategic Finance Center of Excellence

Asher & Company · in joint venture with PwC Interaméricas

psanmartin@asheranalytics.com